Continuous-time Processes¶

The stochastic.processes.continuous module provides classes for generating

discretely sampled continuous-time stochastic processes.

-

class

stochastic.processes.continuous.BesselProcess(dim=1, t=1, rng=None)[source]¶ Bessel process.

The Bessel process is the Euclidean norm of an \(n\)-dimensional Wiener process, e.g. \(\|\mathbf{W}_t\|\)

Generate Bessel process realizations using

dimindependent Brownian motion processes on the interval \([0,t]\)- Parameters

dim (int) – the number of underlying independent Brownian motions to use

t (float) – the right hand endpoint of the time interval \([0,t]\) for the process

rng (numpy.random.Generator) – a custom random number generator

-

sample(n)[source]¶ Generate a realization.

- Parameters

n (int) – the number of increments to generate

-

sample_at(times)[source]¶ Generate a realization using specified times.

- Parameters

times – a vector of increasing time values at which to generate the realization

-

property

t¶ End time of the process.

-

times(n)¶ Generate times associated with n increments on [0, t].

- Parameters

n (int) – the number of increments

-

class

stochastic.processes.continuous.BrownianBridge(b=0, t=1, rng=None)[source]¶ Brownian bridge.

A Brownian bridge is a Brownian motion with a conditional value on the right endpoint of the process.

- Parameters

b (float) – the right endpoint value of the Brownian bridge at time t

t (float) – the right hand endpoint of the time interval \([0,t]\) for the process

rng (numpy.random.Generator) – a custom random number generator

-

property

b¶ Right endpoint value.

-

sample(n)[source]¶ Generate a realization.

- Parameters

n (int) – the number of increments to generate

-

sample_at(times, b=None)[source]¶ Generate a realization using specified times.

- Parameters

times – a vector of increasing time values at which to generate the realization

b (float) – the right endpoint value for

times[-1]

-

property

t¶ End time of the process.

-

times(n)¶ Generate times associated with n increments on [0, t].

- Parameters

n (int) – the number of increments

-

class

stochastic.processes.continuous.BrownianExcursion(t=1, rng=None)[source]¶ Brownian excursion.

A Brownian excursion is a Brownian bridge from (0, 0) to (t, 0) which is conditioned to be nonnegative on the interval [0, t].

Generated using method by

Biane, Philippe. “Relations entre pont et excursion du mouvement Brownien reel.” Ann. Inst. Henri Poincare 22, no. 1 (1986): 1-7.

Vervaat, Wim. “A relation between Brownian bridge and Brownian excursion.” The Annals of Probability (1979): 143-149.

- Parameters

t (float) – the right hand endpoint of the time interval \([0,t]\) for the process

rng (numpy.random.Generator) – a custom random number generator

-

sample(n)[source]¶ Generate a realization.

- Parameters

n (int) – the number of increments to generate.

-

sample_at(times)[source]¶ Generate a realization using specified times.

- Parameters

times – a vector of increasing time values at which to generate the realization

-

property

t¶ End time of the process.

-

times(n)¶ Generate times associated with n increments on [0, t].

- Parameters

n (int) – the number of increments

-

class

stochastic.processes.continuous.BrownianMeander(t=1, rng=None)[source]¶ Brownian meander process.

A Brownian motion conditioned such that the process is nonnegative.

Generated using method by

Williams, David. “Decomposing the Brownian path.” Bulletin of the American Mathematical Society 76, no. 4 (1970): 871-873.

Imhof, J-P. “Density factorizations for Brownian motion, meander and the three-dimensional Bessel process, and applications.” Journal of Applied Probability 21, no. 3 (1984): 500-510.

- Parameters

t (float) – the right hand endpoint of the time interval \([0,t]\) for the process

rng (numpy.random.Generator) – a custom random number generator

-

sample(n, b=None)[source]¶ Generate a realization.

- Parameters

n (int) – the number of increments to generate

b (float) – the nonnegative right hand endpoint of the meander. If not provided, one is randomly selected from a \(\sqrt{2E}\) random variable where \(E\) is exponential.

-

property

t¶ End time of the process.

-

times(n)¶ Generate times associated with n increments on [0, t].

- Parameters

n (int) – the number of increments

-

class

stochastic.processes.continuous.BrownianMotion(drift=0, scale=1, t=1, rng=None)[source]¶ Brownian motion.

A standard Brownian motion (discretely sampled) has independent and identically distributed Gaussian increments with variance equal to increment length. Non-standard Brownian motion includes a linear drift parameter and scale factor.

- Parameters

drift (float) – rate of change of the expected value

scale (float) – scale factor of the Gaussian process

t (float) – the right hand endpoint of the time interval \([0,t]\) for the process

rng (numpy.random.Generator) – a custom random number generator

-

property

drift¶ Drift parameter.

-

sample(n)[source]¶ Generate a realization.

- Parameters

n (int) – the number of increments to generate

-

sample_at(times)[source]¶ Generate a realization using specified times.

- Parameters

times – a vector of increasing time values at which to generate the realization

-

property

scale¶ Scale parameter.

-

property

t¶ End time of the process.

-

times(n)¶ Generate times associated with n increments on [0, t].

- Parameters

n (int) – the number of increments

-

class

stochastic.processes.continuous.CauchyProcess(t=1, rng=None)[source]¶ Symmetric Cauchy process.

The symmetric Cauchy process is a Brownian motion with a Levy subordinator using location parameter 0 and scale parameter \(t^2/2\).

- Parameters

t (float) – the right hand endpoint of the time interval \([0,t]\) for the process

rng (numpy.random.Generator) – a custom random number generator

-

sample(n)[source]¶ Generate a realization.

- Parameters

n (int) – the number of increments to generate.

-

sample_at(times)[source]¶ Generate a realization using specified times.

- Parameters

times – a vector of increasing time values at which to generate the realization

-

property

t¶ End time of the process.

-

times(n)¶ Generate times associated with n increments on [0, t].

- Parameters

n (int) – the number of increments

-

class

stochastic.processes.continuous.FractionalBrownianMotion(hurst=0.5, t=1, rng=None)[source]¶ Fractional Brownian motion process.

A fractional Brownian motion (discretely sampled) has correlated Gaussian increments defined by Hurst parameter \(H\). When \(H = 1/2\), the process is a standard Brownian motion. When \(H > 1/2\), the increments are positively correlated. When \(H < 1/2\), the increments are negatively correlated.

Hosking’s method:

Hosking, Jonathan RM. “Modeling persistence in hydrological time series using fractional differencing.” Water resources research 20, no. 12 (1984): 1898-1908.

Davies Harte method:

Davies, Robert B., and D. S. Harte. “Tests for Hurst effect.” Biometrika 74, no. 1 (1987): 95-101.

- Parameters

hurst (float) – the Hurst parameter on the interval (0, 1)

t (float) – the right hand endpoint of the time interval \([0,t]\) for the process

rng (numpy.random.Generator) – a custom random number generator

-

property

hurst¶ Hurst parameter.

-

sample(n)[source]¶ Generate a realization.

- Parameters

n (int) – the number of increments to generate

-

property

t¶ End time of the process.

-

times(n)¶ Generate times associated with n increments on [0, t].

- Parameters

n (int) – the number of increments

-

class

stochastic.processes.continuous.GammaProcess(mean=None, variance=None, rate=None, scale=None, t=1, rng=None)[source]¶ Gamma process.

A Gamma process (discretely sampled) is the summation of stationary independent increments which are distributed as gamma random variables. This class supports instantiation using the mean/variance parametrization or the rate/scale parametrization.

- Parameters

mean (float) – mean increase per unit time; supply with

variancevariance (float) – variance of increase per unit time; supply with

meanrate (float) – the rate of jump arrivals; supply with

scalescale (float) – the size of the jumps; supple with

ratet (float) – the right hand endpoint of the time interval \([0,t]\) for the process

rng (numpy.random.Generator) – a custom random number generator

-

property

mean¶ Mean increase per unit time.

-

property

rate¶ Rate of jump arrivals.

-

sample(n)[source]¶ Generate a realization.

- Parameters

n (int) – the number of increments to generate

-

sample_at(times)[source]¶ Generate a realization at specified times.

- Parameters

times – a vector of increasing time values at which to generate the realization

-

property

scale¶ Scale parameter for jump sizes.

-

property

t¶ End time of the process.

-

times(n)¶ Generate times associated with n increments on [0, t].

- Parameters

n (int) – the number of increments

-

property

variance¶ Variance of increase per unit time.

-

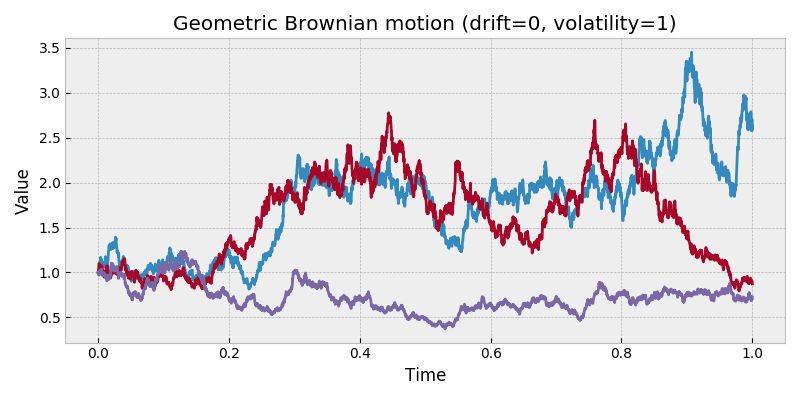

class

stochastic.processes.continuous.GeometricBrownianMotion(drift=0, volatility=1, t=1, rng=None)[source]¶ Geometric Brownian motion process.

A geometric Brownian motion \(S_t\) is the analytic solution to the stochastic differential equation with Wiener process \(W_t\):

\[dS_t = \mu S_t dt + \sigma S_t dW_t\]and can be represented with initial value \(S_0\) in the form:

\[S_t = S_0 \exp \left( \left( \mu - \frac{\sigma^2}{2} \right) t + \sigma W_t \right)\]- Parameters

drift (float) – the parameter \(\mu\)

volatility (float) – the parameter \(\sigma\)

t (float) – the right hand endpoint of the time interval \([0,t]\) for the process

rng (numpy.random.Generator) – a custom random number generator

-

property

drift¶ Geometric Brownian motion drift parameter.

-

sample(n, initial=1)[source]¶ Generate a realization.

- Parameters

n (int) – the number of increments to generate.

initial (float) – the initial value of the process \(S_0\).

-

sample_at(times, initial=1)[source]¶ Generate a realization using specified times.

- Parameters

times – a vector of increasing time values at which to generate the realization

initial (float) – the initial value of the process \(S_0\).

-

property

t¶ End time of the process.

-

times(n)¶ Generate times associated with n increments on [0, t].

- Parameters

n (int) – the number of increments

-

property

volatility¶ Geometric Brownian motion volatility parameter.

-

class

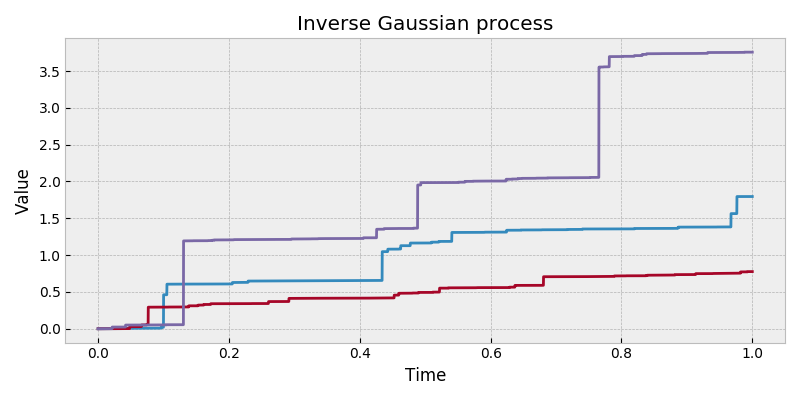

stochastic.processes.continuous.InverseGaussianProcess(mean=None, scale=1, t=1, rng=None)[source]¶ Inverse Gaussian process.

An inverse Gaussian process has independent increments which follow an inverse Gaussian distribution with parameters defined by a monotonically increasing function, \(\Gamma(t)\). E.g. for increment \([s, t]\):

\(\mathcal{IG}(\Gamma(t) - \Gamma(s), \eta(\Gamma(t) - \Gamma(s))^2)\)

Uses a method for generating inverse Gaussian variates from:

Michael, John R., William R. Schucany, and Roy W. Haas. “Generating random variates using transformations with multiple roots.” The American Statistician 30, no. 2 (1976): 88-90.

- Parameters

mean (callable) – a callable with one argument \(\Gamma(t)\) such that \(\Gamma(t') > \Gamma(t) \forall t' > t\). Default is the identity function.

scale (float) – scale factor of the shape parameter of the inverse gaussian, or \(\eta\) from the above equation.

t (float) – the right hand endpoint of the time interval \([0,t]\) for the process

rng (numpy.random.Generator) – a custom random number generator

-

property

mean¶ Mean function.

-

sample(n)[source]¶ Generate a realization.

- Parameters

n (int) – the number of increments to generate

-

sample_at(times)[source]¶ Generate a realization using specified times.

- Parameters

times – a vector of increasing time values at which to generate the realization

-

property

scale¶ Scale parameter.

-

property

t¶ End time of the process.

-

times(n)¶ Generate times associated with n increments on [0, t].

- Parameters

n (int) – the number of increments

-

class

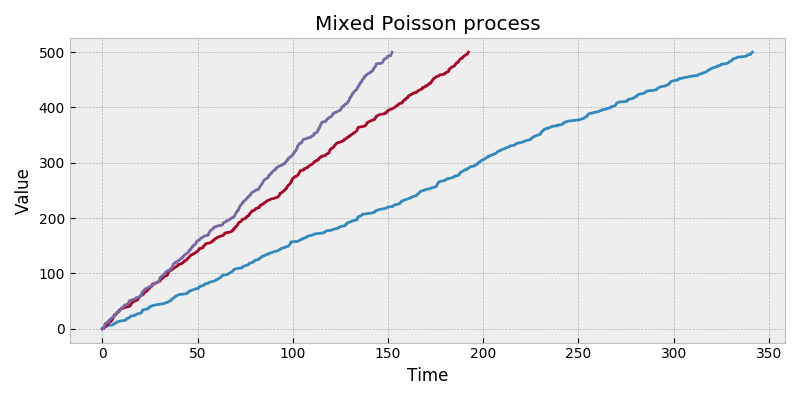

stochastic.processes.continuous.MixedPoissonProcess(rate_func, rate_args=None, rate_kwargs=None, rng=None)[source]¶ Mixed poisson process.

A mixed poisson process is a Poisson process for which the rate is a scalar random variate. The sample method will generate a random variate for the rate before generating a Poisson process realization with the rate. A Poisson process with rate \(\lambda\) is a count of occurrences of i.i.d. exponential random variables with mean \(1/\lambda\). Use the

rateattribute to get the most recently generated random rate.- Parameters

rate_func (callable) – a callable to generate variates of the random rate

rate_args (tuple) – positional args for

rate_funcrate_kwargs (dict) – keyword args for

rate_funcrng (numpy.random.Generator) – a custom random number generator

-

property

rate¶ The most recently generated rate.

Attempting to get the rate prior to generating a sample will raise an

AttributeError.

-

property

rate_args¶ Positional arguments for the rate function.

-

property

rate_func¶ Current rate’s distribution.

-

property

rate_kwargs¶ Keyword arguments for the rate function.

-

sample(n=None, length=None)[source]¶ Generate a realization.

Exactly one of n and length must be provided. Generates a random variate for the rate, then generates a Poisson process realization using this rate.

- Parameters

n (int) – the number of arrivals to simulate

length (int) – the length of time to simulate; will generate arrivals until length is met or exceeded.

-

class

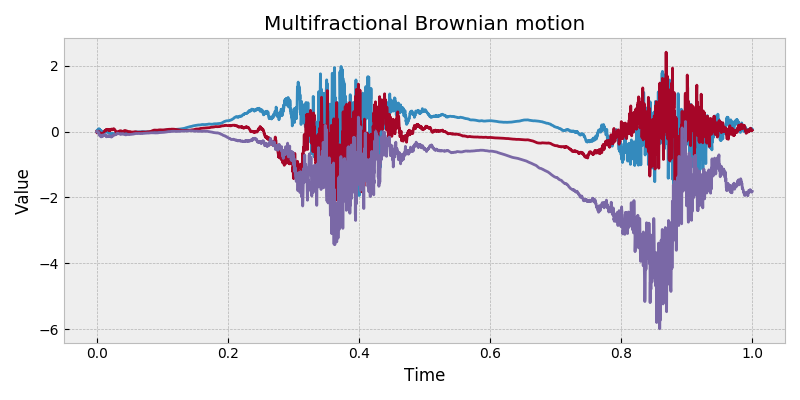

stochastic.processes.continuous.MultifractionalBrownianMotion(hurst=None, t=1, rng=None)[source]¶ Multifractional Brownian motion process.

A multifractional Brownian motion generalizes a fractional Brownian motion with a Hurst parameter which is a function of time, \(h(t)\). If the Hurst is constant, the process is a fractional Brownian motion. If Hurst is constant equal to 0.5, the process is a Brownian motion.

Approximate method originally proposed for fBm in

Rambaldi, Sandro, and Ombretta Pinazza. “An accurate fractional Brownian motion generator.” Physica A: Statistical Mechanics and its Applications 208, no. 1 (1994): 21-30.

Adapted to approximate mBm in

Muniandy, S. V., and S. C. Lim. “Modeling of locally self-similar processes using multifractional Brownian motion of Riemann-Liouville type.” Physical Review E 63, no. 4 (2001): 046104.

- Parameters

hurst (float) – a callable with one argument \(h(t)\) such that \(h(t') \in (0, 1) \forall t' \in [0, t]\). Default is \(h(t) = 0.5\).

t (float) – the right hand endpoint of the time interval \([0,t]\) for the process

rng (numpy.random.Generator) – a custom random number generator

-

property

hurst¶ Hurst function.

-

sample(n)[source]¶ Generate a realization.

- Parameters

n (int) – the number of increments to generate

-

property

t¶ End time of the process.

-

times(n)¶ Generate times associated with n increments on [0, t].

- Parameters

n (int) – the number of increments

-

class

stochastic.processes.continuous.PoissonProcess(rate=1, rng=None)[source]¶ Poisson process.

A Poisson process with rate \(\lambda\) is a count of occurrences of i.i.d. exponential random variables with mean \(1/\lambda\). This class generates samples of times for which cumulative exponential random variables occur.

- Parameters

rate (float) – the parameter \(\lambda\) which defines the rate of occurrences of the process

rng (numpy.random.Generator) – a custom random number generator

-

property

rate¶ Rate parameter.

-

class

stochastic.processes.continuous.SquaredBesselProcess(dim=1, t=1, rng=None)[source]¶ Squared Bessel process.

The square of a Bessel process: \(\|\mathbf{W}_t\|^2\).

The Bessel process is the Euclidean norm of an \(n\)-dimensional Wiener process, e.g. \(\|\mathbf{W}_t\|\)

- Parameters

dim (int) – the number of underlying independent Brownian motions to use

t (float) – the right hand endpoint of the time interval \([0,t]\) for the process

-

property

dim¶ Dimensions, or independent Brownian motions.

-

sample(n)[source]¶ Generate a realization.

- Parameters

n (int) – the number of increments to generate

-

sample_at(times)[source]¶ Generate a realization using specified times.

- Parameters

times – a vector of increasing time values at which to generate the realization

-

property

t¶ End time of the process.

-

class

stochastic.processes.continuous.VarianceGammaProcess(drift=0, variance=1, scale=1, t=1, rng=None)[source]¶ Variance Gamma process.

A variance gamma process has independent increments which follow the variance-gamma distribution. It can be represented as a Brownian motion with drift subordinated by a Gamma process:

\[\theta \Gamma(t; 1, \nu) + \sigma W(\Gamma(t; 1, \nu))\]- Parameters

drift (float) – the drift parameter of the Brownian motion, or \(\theta\) above

variance (float) – the variance parameter of the Gamma subordinator, or \(\nu\) above

scale (float) – the scale parameter of the Brownian motion, or \(\sigma\) above

t (float) – the right hand endpoint of the time interval \([0,t]\) for the process

rng (numpy.random.Generator) – a custom random number generator

-

property

drift¶ Drift parameter.

-

sample(n)[source]¶ Generate a realization.

- Parameters

n (int) – the number of increments to generate

-

sample_at(times)[source]¶ Generate a realization using specified times.

- Parameters

times – a vector of increasing time values at which to generate the realization

-

property

scale¶ Scale parameter.

-

property

t¶ End time of the process.

-

property

variance¶ Variance parameter.

-

class

stochastic.processes.continuous.WienerProcess(t=1, rng=None)[source]¶ Wiener process, or standard Brownian motion.

- Parameters

t (float) – the right hand endpoint of the time interval \([0,t]\) for the process

rng (numpy.random.Generator) – a custom random number generator

-

sample(n)¶ Generate a realization.

- Parameters

n (int) – the number of increments to generate

-

sample_at(times)¶ Generate a realization using specified times.

- Parameters

times – a vector of increasing time values at which to generate the realization

-

property

t¶ End time of the process.

-

times(n)¶ Generate times associated with n increments on [0, t].

- Parameters

n (int) – the number of increments